Serviços Personalizados

Journal

Artigo

Inglês (pdf)

Inglês (pdf)

Artigo em XML

Artigo em XML Referências do artigo

Referências do artigo

Enviar este artigo por email

Enviar este artigo por emailIndicadores

-

Citado por SciELO

Citado por SciELO -

Acessos

Acessos

Links relacionados

-

Similares em

SciELO

Similares em

SciELO

Compartilhar

Permalink

PermalinkTourism & Management Studies

versão impressa ISSN 2182-8458

TMStudies vol.10 no.Especial Faro dez. 2014

MANAGEMENT - SCIENTIFIC PAPERS

Creating a holistic excellence model adapted for technology-based companies

Creación de un modelo de excelencia holístico adaptado empresas de base tecnológica

Ana Clara Pastor Tejedor1; Jesús Pastor Tejedor2; Luis Navarro Elola3; Manbir Sodhi4; Guillermo Pérez Sancho5

1School of Engineering and Architecture, University of Zaragoza, Department of Organisation and Business Management, C/María de Luna, 3 50018 Zaragoza. Spain, acpastor@unizar.es

2School of Engineering and Architecture, University of Zaragoza, Department of Organisation and Business Management, C/María de Luna, 3 50018 Zaragoza. Spain, jpastej@unizar.es

3School of Engineering and Architecture, University of Zaragoza, Department of Organisation and Business Management, C/María de Luna, 3 50018 Zaragoza. Spain, lnavarro@unizar.es

4University of Rhode Island, Department of Mechanical Systems and Industrial Engineering, 103A Gilbreth Hall 2 East Alumni Ave. Kingston, RI 02881 EEUU, sodhi@egr.uri.edu

5School of Engineering and Architecture, University of Zaragoza, Department of Organisation and Business Management, C/María de Luna, 3 50018 Zaragoza. Spain, gperezsancho@gmail.com

ABSTRACT

The objective of this study is the preparation of a management model that brings together the advantages of models from different disciplines: Balanced Scorecard (BSC), European Foundation for Quality Management (EFQM) and Holistic Marketing (HM).

HM proposes an overview of organisations – taking into account all value streams which companies generate – while the business excellence criteria of the EFQM define the structure platforms of Kotler et al. (2001), and the BSC guarantees implementation, monitoring and enforcement.

Once developed, this model was adapted for the specific characteristics of technology-based companies (TBC), based on interviews with managers of these businesses.

Keywords: Management, marketing, quality, BSC, EFQM

RESUMEN

El objetivo de este estudio es la confección de un modelo de gestión que aglutine las ventajas de modelos de distintas disciplinas: Balanced Scored Card (BSC), Modelo Europeo de Gestión de la Calidad (EFQM) y Marketing Holístico (MH).

Una vez desarrollado este modelo se adaptó a las características particulares de las empresas de base tecnológica (ETBs), basándonos en dieciocho entrevistas realizadas a gerentes de este tipo de empresas.

Palabras-clave: Gestión, marketing, calidad, BSC, EFQM

1. Introduction

At present, most organisations have the need to use a comprehensive management model which, based on a scheme or framework, helps them manage their organisations and achieve quantitative and qualitative objectives or goals both in the short and long term.

Organisations have to survive in a highly competitive, unstable and changeable environment. Only those companies able to adapt themselves quickly to the demands of today's society will succeed, thus becoming sustainable companies which are flexible in the face of environment changes.

For this reason, it is relevant to develop a management model which comprises the advantages of the most widely used and accepted organisational models, minimising the weaknesses that may appear when implementing a single model. Therefore, this study proposes the Holistic Marketing (HM) framework (Kotler et al., 2001) as a base on which to integrate the last revision of the European Foundation for Quality Management Excellence Model (EFQM, 2010) and the Balanced Scorecard (BSC) strategic management model (Kaplan & Norton, 1996).

To maximise the efficiency of our model, we conducted a literature review on the latest strategic planning models and obtained information from eighteen interviews with managers of technology-based companies who shared their expertise in this area.

2. Literature review

Technology-based companies are a fast-growing sector in the Spanish economy. Therefore, this research attempts to define a model to identify key initiatives and processes to successfully introduce positioning and growth strategies for technology-based companies.

The Office of Technology Assessment defined technology-based companies as organisations providing both products and services committed to the design, development and production of innovative products and/or manufacturing processes through the systematic application of technological and scientific knowledge (Asociación Nacional de Centros Europeos de Empresas Innovadoras Españoles, 2008).

Once we had selected the type of business as the scope of our study, we could confirm that they have to compete in an business environment characterised by high competitiveness, fast technological advances and reduced timelines, combined with the development of powerful initiatives of collaboration among organisations such as networking, strategic alliances and outsourcing. Discoveries of new distribution lines (based on the Internet) and e-commerce trends, B2B (business to business) and B2C (business to consumer) have created new horizons and channels open to development and strongly positioning technology-based products.

Among the different possible models, the proposed management system used in this study is based on the HM approach by Kotler et al. (2001), due to this sector’s special interest in new opportunities that new technologies offer to companies which want to grow sustainably.

During the last three decades, companies around the world have experienced the development and spread of a group of non-technological innovations designed to improve management performance in organisations. One of them is quality management (Bayo Moriones et al., 2011). For this reason, one of the models comprised in the proposed management system is the EFQM, which allows us to both fix a specific strategy and manage an organisation from a quality point of view, showing us the distance remaining before excellence is achieved. Furthermore, according to Rezaei et al. (2011), the implementation of a quality system allows us to be highly effective in creating personal motivation as a result of developing a competitive environment and encouraging staff to take responsibility for enhancing productivity, reducing costs and increasing profits.

By integrating only the EFQM with HM, we cannot establish a link between the improvement of local processes (mostly operational improvement) and the improvement of results from perspectives such as financial or customer viewpoints. However, the BSC establishes a cause-effect relationship between enablers and results (Pastor, 2008).

The integration of this third model helps complete and optimise strategic management and planning, and it is an assessment tool, allowing completion and review of management from a different point of view. As Pastor Tejedor (2008) proposes, BSC methodology also integrates our model with other management processes performed in a company.

The implementation of quality management models in companies not only improves quality but also increases market share, customer satisfaction, profits, business processes, provider performance, employee morale and competitiveness (Cauchick et al., 2004).

The BSC includes a group of measures to monitor organisational performance from four perspectives. The advantage of this model is that a series of indicators is at the disposal of senior managers. Moreover, this complementary tool translates into strategic orientations, giving everyone in the organisation a better understanding (Mantegui & Zohrabi, 2011).

Therefore, by integrating the EFQM and BSC into the HM approach, overall strategy can be defined with high success. The EFQM helps organisations to develop their strategic planning and the BSC warrants compliance, monitoring and implementation.

The BSC introduces four perspectives on business performance to measure business excellence and quality: financial, customer, internal business process, and learning and growth. Thus it supports a holistic approach as it does not take into account only one aspect of a company but the company as a whole.

Kanji (2002) criticised this model because it does not identify the contributions of the most important stakeholders, so the BSC can be improved by including the principles of Total Quality Management (TQM) and other key indicators to successfully measure performance. Thus, Kanji's model (2002), termed Kanji's Business Excellence Model (KBEM), while based on the BSC system also includes a multi-perspective vision of quality measurement so that business results are measured from both a financial and nonfinancial point of view.

In the same way, other analysed models constructed by Yang (2002) and León-Soriano et al. (2010) measure business performance not only from a financial dimension but also from different perspectives. The framework proposed by Yang consists of the BSC, strategic planning and the Hoshin Management method in an integrated model where the BSC is the main construct. Therefore, the idea of using the BSC as a tool for strategic compliance, monitoring and application within our proposed Holistic Excellence Model is also validated by Yang's model.

On the other hand, the model proposed by León-Soriano et al. (2010) consists of a series of phases which the company has to go through to achieve sustainable planning and management strategies by the implementation of a sustainable BSC (SBSC). In this sense, the BSC is kept, like in the previous models, as the main construct.

For this reason, we consider the three analysed models above – those of Kanji, Yang and León-Soriano et al. – to have a common starting point: the BSC and its holistic approach to companies.

Despite similarities, their contributions are different from each other. Kanji's model (2002), as mentioned before, attempts to improve the BSC by stressing the most important stakeholders, in such a way that in the process of implementing the KBEM model, the information on measured indicators of business excellence is provided by each interested group in the company, that is, the stakeholders (customers, providers, government, staff, and so on). In fact, the aim of this paper is to incorporate business performance into a system which measures results from the stakeholders' perspective. For that reason, one of the organisational indicators that measure this model is stakeholder satisfaction, meeting stakeholders’ needs and expectations.

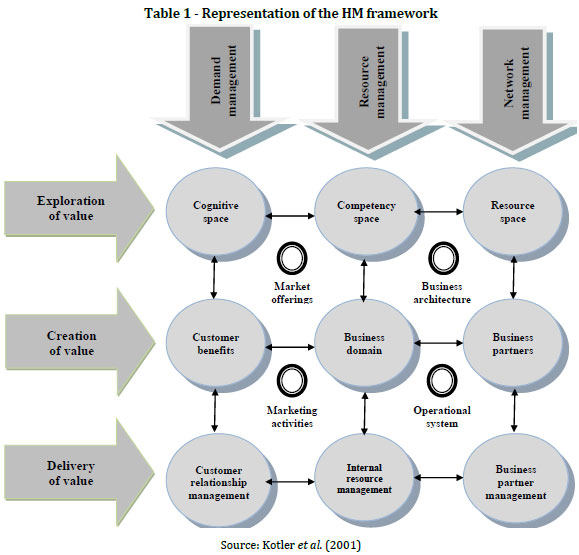

If we compare the organisational value of the KBEM to the HM model, represented schematically in Table 1, it is apparent that there is some relationship between both. Thus, the measurement of stakeholder satisfaction in the KBEM is very similar to customer satisfaction included under customer benefits in the HM framework. However, obviously the KBEM not only takes into account customers but also all stakeholders since, as pointed out above, this is precisely its main contribution.

On the other hand, Yang's model (2009), which also uses the BSC as its main focus, was developed because of the limitation of resources in companies (theory of resources). Yang states that, due to a shortage of resources, companies cannot implement all quality measurement systems and, therefore, a system model that integrates several systems is needed to maximise the opportunities of business assessment. To do this, Yang introduces a model which incorporates the BSC, strategic planning and the Hoshin Management method, thus integrating these three systems and resulting in a more powerful measurement tool than the three tools alone.

In this model, there is less emphasis on stakeholders, but the BSC does take customers into account. In Hoshin Management, different departments or units in a company are analysed, so employees are taken into consideration. Strategic planning analyses the environment, so other stakeholders such as the government or society can thus be taken into account while measuring company quality.

Regarding the Hoshin Management tool, there are similarities to the model of León-Soriano et al. such as the element of strategic planning, as mentioned above, which analyses the environment of a company comprised of, among others, society or the environment. Thus, the SBSC as proposed by León-Soriano et al. (2010) is a system of measuring business excellence that allows a sustainable economy (taken into account in the previous models) and, moreover, ecological and social sustainability (the main contribution of this model and which was previously included in strategic planning by Yang).

Thus, the SBSC model consists of the BSC (also present in the other models), strategic planning (as in Yang's model), and information systems in other research areas.

In this way, and as the authors state, the SBSC not only takes into account stockholders (financial perspective of quality measurement) but also all the stakeholders of a company. We can see, thus, the relationship between the SBSC and the KBEM models.

Another similarity between the SBSC model and the previous ones is its implementation which proposes a "step by step" process. Although the definition of the steps to follow is more detailed in this last model, the previous models analysed in this study also require sequential execution of tasks for a successful implementation.

Finally, other notable similarities among the models is the identification of values, mission and/or vision as one of the first steps to the implementation of the system of measuring business excellence, as well as the linking of strategy and objectives so that the different departments and units of the company are coherent and satisfy all the stakeholders' needs and expectations, not just shareholders’.

After studying the similarities, differences and potential links among the BSC, the KBEM (Kanji's model), Yang's model, the EFQM, the HM framework and the SBSC (the León-Soriano et al. model), we propose the development of a Holistic Excellence Model adapted for technology-based companies.

There are currently several strategic planning processes and tools whose efficiency and effectiveness vary from one company to another (Tohidi et al., 2010). To get better results, the model proposed in this study can be adapted both for the specific characteristics of each company (from big to small organisations) and for the environment where they operate.

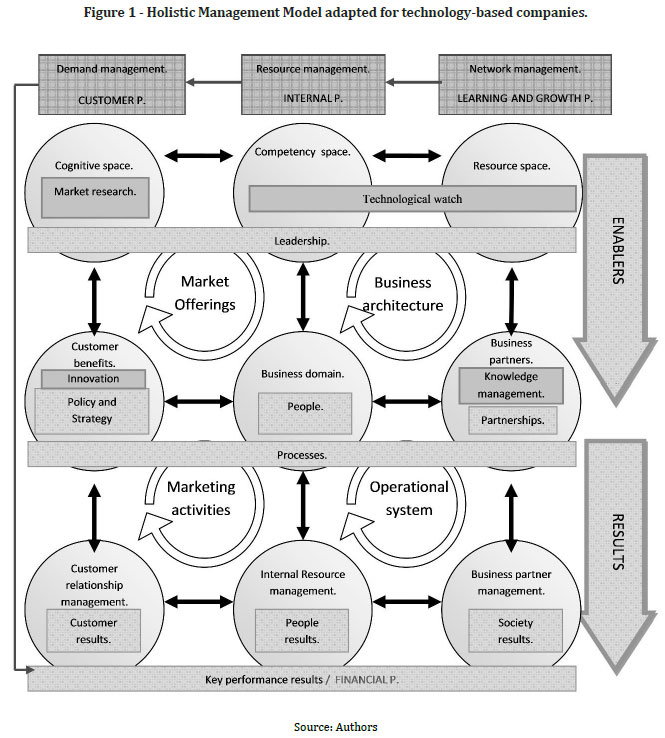

Figure 1 represents the management model proposed in this study, which integrates the BSC (in rectangles) and the different factors in the EFQM (in circles) into the HM framework. Thus, we can observe HM is compatible with the other two models and the three of them complement one another. The contributions gathered through our review of the literature have been taken into account to improve the Holistic Excellence Model proposed in this paper.

The contribution of Kanji’s Business Excellence Model to the model proposed by Kotler et al. (2001) is the definition of the structure of the HM operational and strategic platforms, by allocating the thirty-two sub-criteria for self-assessment from Kanji’s Business Excellence Model to the nine value streams proposed by Kotler et al. in their approach.

In this study, this distribution of values is compared with the value given by managers of technology-based companies to these platforms, based on eighteen interviews with managers from different companies.

3. Method

Kotler et al. (2001) divide the value stream of every organisation into three value drivers depending on the philosophy of the business. These are customer values, core competencies and collaborative networks. Their research also establishes three phases in each value stream: value exploration, value creation and value delivery. The vision of Kotler et al. is enriching, visual and clear. However, in order to use this model as a strategic planning tool, the guidelines and methods used to achieve value exploration, value creation and value delivery need to be defined, through the integration of the EFQM and the BSC approaches in our measurement system.

In order to guarantee the validity of our proposed model, this study had to verify that the following hypotheses are confirmed:

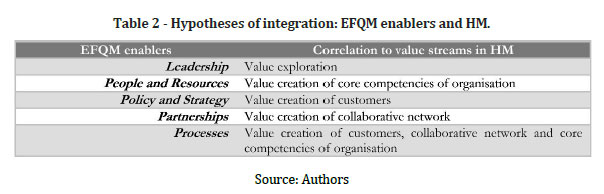

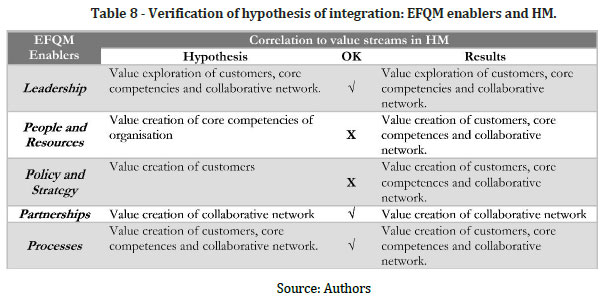

Hypothesis 1. As Table 2 shows, there is a parallel structure between value exploration and value creation in the HM approach and enablers in the EFQM.

If we analyse enablers in the EFQM, Leadership should perfectly fit into the phase that Kotler et al. define as value exploration, and the enabler labelled Processes falls within value creation. At the same time, we verify that the Policy and Strategy enablers coincide with value creation within the customer focus, the enablers People and Resources coincide with value creation within the core competencies, and the Partnerships enabler coincides with value creation within the collaborative network.

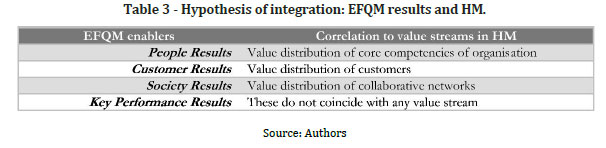

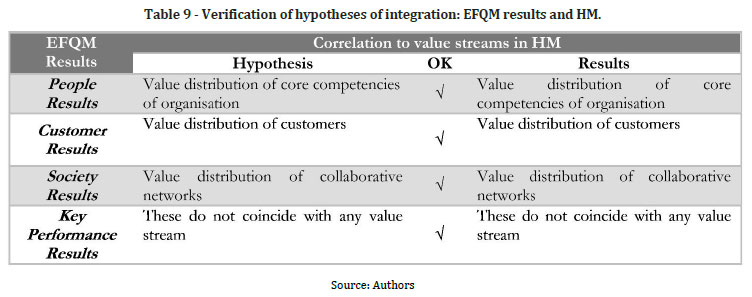

Hypothesis 2. As Table 3 shows, there is a clear correlation between value delivery and EFQM results.

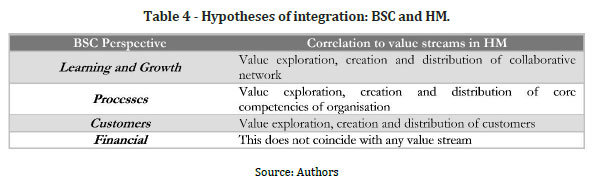

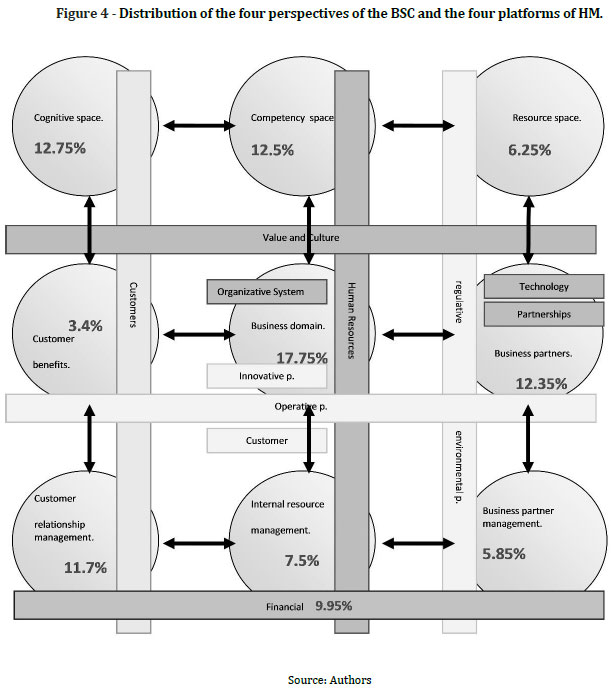

Hypothesis 3. As Table 4 shows, the three value streams in the HM approach (focused on customer, core competencies and collaborative network) coincide with three perspectives in the BSC: Customer, Internal Processes, and Learning and Growth.

Hypothesis 4. As Table 5 shows, there is a coincidence between Key Performance Results of the EFQM and the Financial perspective of the BSC. This shows how the organisation has been managed in previous periods.

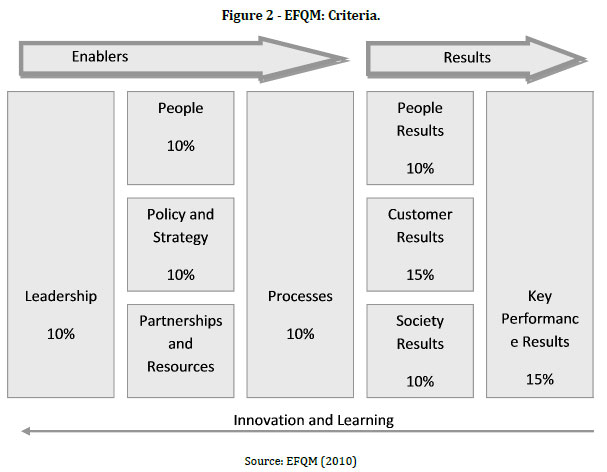

The EFQM evaluates organisations on the basis of nine criteria and assigns a weight or percentage of responsibility for the success of organisations as illustrated in Figure 2. These nine criteria of the EFQM, used to define how the organisation approaches excellence, are divided into thirty-two criteria.

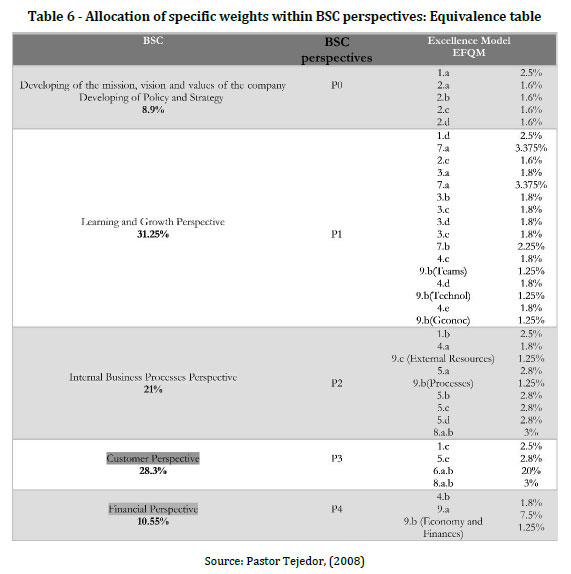

Pastor Tejedor (2008) allocated these sub-criteria within each BSC perspective. Through this allocation, the author was able to assign a specific weight to each perspective, as illustrated in Table 6.

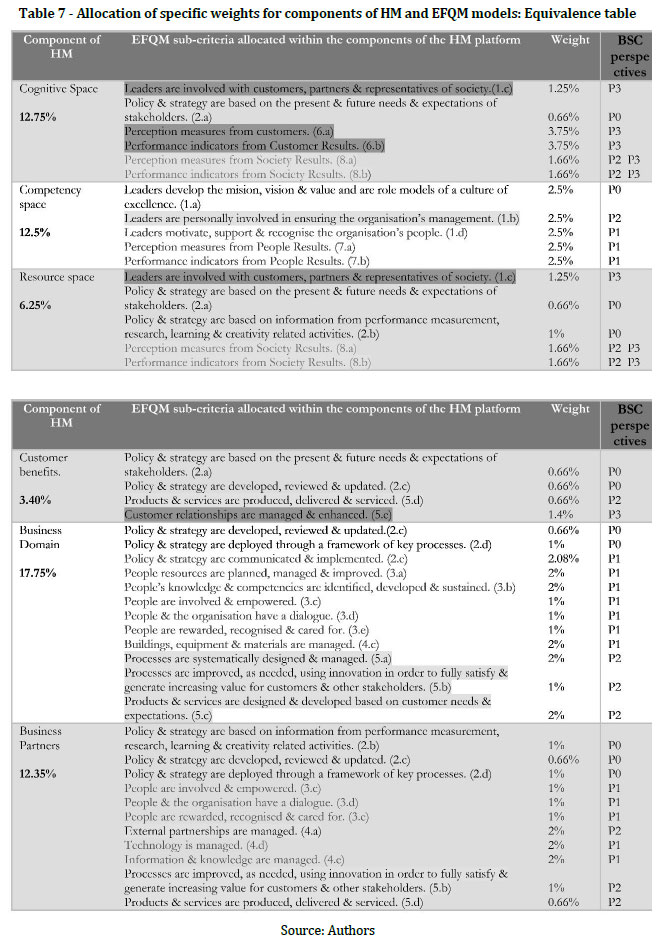

The sub-criteria of the EFQM have been allocated within the components of the four platforms of the HM approach, determining the weight or percentage of responsibility of each part in the success of the company, as illustrated in Table 7.

4. Results

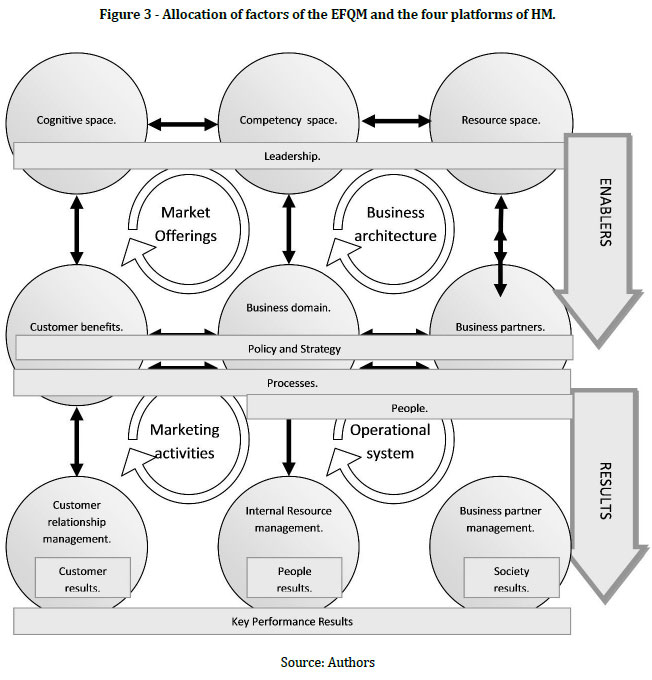

As a consequence of the allocation of the sub-criteria within the nine value streams of the HM approach, the factors of the EFQM are distributed into the four platforms, as illustrated in Figure 3. As illustrated in Table 8 and Figure 3, if we analyse how the enablers of the EFQM have been allocated, we can see not all the hypotheses tested are proved.

However, as illustrated in Table 9, if we test the hypotheses on the results of the EFQM, we can see all are proved.

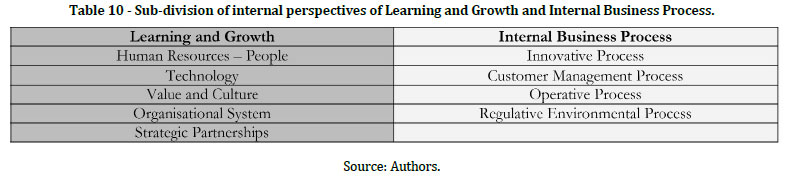

We can see enablers of the EFQM coincide with strategic platforms, whereas results coincide with operational platforms. In analysing the EFQM, results are the result of enablers and, therefore, Marketing Activities and Operational System are the result of Business Architecture and Market Offerings. The four perspectives of the BSC are distributed within the nine value streams of the HM approach, as illustrated in Figure 4 below. As we can see in Table 10, the internal perspectives of Learning and Growth and the Internal Business Process are sub-divided as follows:

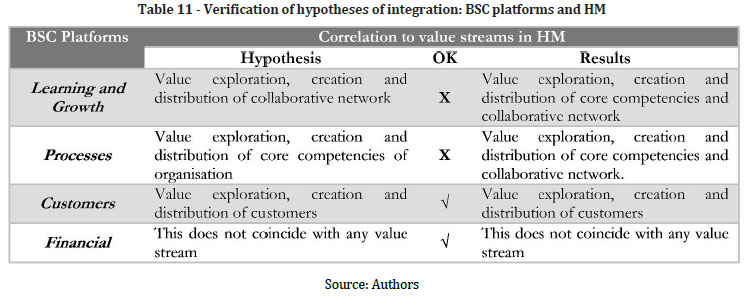

As Table 11 shows, if we compare the previous hypothesis tested on the distribution of the BSC platforms within the HM approach, we verify not all of them prove to be right.

The right column shows the weight of value exploration, creation and distribution of the collaborative network. This column reflects the concept of “co-makership”. This value stream helps organisations to improve and enhance stable partnerships and alliances between all relevant members, from providers to costumers, in order to integrate all resource and information streams and in this way obtain sustainable advantages in the market.

This concept goes further to focus on everything related to co-development, co-design, co-improvement, and co-management: in other words, a common way forward which is absolutely integrated.

Most of the differences seen in managers’ evaluations of technology-based companies regarding the theoretical calculation of weight are:

- value exploration of collaborative networks

- value creation of customer focus

Managers in this type of company show the same interest as others in understanding and meeting customers’ needs but, in contrast to other organisations, they recognise a greater worth of value creation for customers, above that of the worth given in the theoretical model.

They also give special importance to value exploration of collaborative networks where they exchange information, knowledge and co-development of projects.

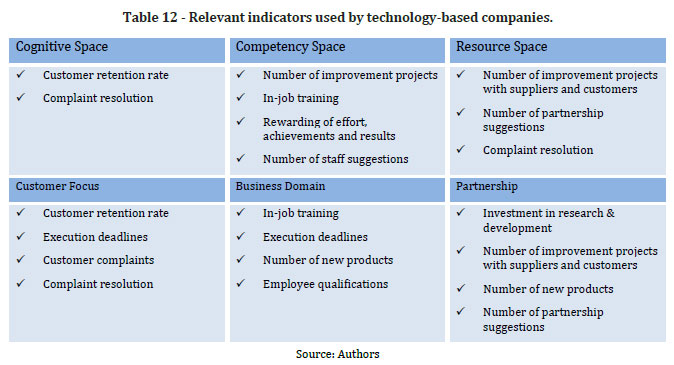

Due to the specific characteristics of these companies and their external environments, managers of technology-based companies have contributed the following group of indicators to identify their organisations’ state and if they are achieving their assigned objectives:

5. Conclusions

Our model visually describes different value streams generated by companies, with an emphasis on main aspects of new technologies organisations.

The model proposed in this paper integrates the EFQM, which can help organisations identify their weaknesses as they approach excellence. On the basis of this information, the strategy of an organisation can be defined.

In turn, integration of the BSC can help the implementation, compliance and monitoring of this strategy by the definition of some indicators.

By integrating both the EFQM and BSC within the HM approach, we conclude:

- There is a relationship between HM's strategy platforms and EFQM's enablers.

- There is a relationship between HM's operational platforms and EFQM's results.

- BSC's perspectives can be distributed within HM's value streams.

- The weight of each of the HM's value streams can be determined.

Through the integration of the BSC and the EFQM within the HM framework, we could determine the cause-effect relationships among the different HM's platforms.

By establishing these cause-effect relationships in our study, we conclude that the first platform to be defined and enhanced in the strategic planning process should be Business Architecture. Therefore, based on the Open Innovation Theory (Igea, 2011), we recommend:

- Assessing Core Competencies by describing main needs and relevant performance principles.

- Restructuring Business Domains on the basis of new technologies by listing the steps to follow and the best initiatives for value creation.

- Understanding Resource Spaces through the most efficient performance principles.

- Enlarging Partnership Spaces through the description of relevant relationships among organisations and the best initiatives for value creation for Collaborative Networks.

The benefits of enhancing Business Architecture can be seen in Market Offerings and Operational System platforms. Similarly, the benefits of developing these platforms can be seen in the Marketing Activities platform.

We include here all the results and processes followed to calculate the weight of each HM platform based on the weight of each EFQM enabler and result. In this way, companies are aware of the importance of each factor in their organisations’ global success and how they contribute to the consistent distribution of resources.

Through the theoretical allocation carried out in this study, we conclude the weighting of strategic platforms is higher than operational platforms in achieving excellence. Market Offerings receive the greatest weight, which reflects the contribution of the EFQM to sustainability and developing customer loyalty.

Each manager interviewed for this study evaluated the model and each sub-criterion as implemented in their companies. Through the information obtained from their evaluations, we conclude that companies are aware of the importance of the different excellence criteria but do not always meet their goals. This is partly explained by the fact that they do not have clear performance plans which prioritise some actions over others. This weakness can be solved through the excellence model proposed in this study because, as we mentioned before, the HM framework enables a global analysis of organisations while the EFQM helps develop a strategy and the BSC guarantees its implementation.

The development of their Business Architecture platforms helps companies obtain competitive advantages over their competitors. According to the interviewed managers, the Business Domain platform is the furthest away from meeting their objectives. This platform should be maximised by internal Research & Development enhancement, in-job training and a positive attitude towards making risky decisions.

Based on the importance given by each manager to each of the excellence criterion, we calculated the weight of each value stream. According to this, value creation for core competencies decreases its weight against value creation for customers. This illustrates the dependence of companies interviewed on their customers and how they focus on acknowledging and meeting customer needs in order to ensure their loyalty.

The result of this study is a Holistic Excellence Model which integrates the advantages of systems widely used today. It was evaluated by eighteen companies and can be applied and adapted for each organisation's needs, enabling companies to evaluate their strategic planning and implementation, as shown for the technology-based companies studied.

References

Bayo Moriones, A., Merino D. C. J. & Selvam, R. M. (2011). The impact of Iso 9000 and EFQM on the use of flexible work practices. International Journal of Production Economics, 130(1), 33-42. [ Links ]

Cauchick, M., Morini, C. & Pires, S. (2004). An application case of the Brazilian National Quality Award. The Tqm Magazine, 16(3), 186-193. [ Links ]

EFQM. (2010). Guía para la transición. Cómo actualizarse al modelo EFQM de excelencia 2010. Retrieved December 21, 2012 from http://www.efqm.org [ Links ]

Igea García, M. (2011). Estudio de la aplicación del modelo de negocio de open innovation en pequeñas y medianas empresas en el ámbito tecnológico y de la ingeniería. Proyecto non publicado de fin de carrera escuela de ingeniería y arquitectura, Universidad de Zaragoza, Zaragoza, España. [ Links ]

Kanji, G. K. (2002). Business excellence: Make it happen. Total Quality Management, 13(8), 1115-1124. [ Links ]

Kaplan, R. & Norton, D. (1996). The balanced scorecard: Translating Strategy into action. Boston: Harvard Business Press. [ Links ]

Kotler, P., Jain, D.C. & Maesincee, S. (2001). Marketing moves. A new approach to profit, growth, and renewal. Boston: Harvard Business Press. [ Links ]

León-Soriano, R., Muñoz-Torres, M. J. & Chalmeta-Rosaleñ, R. (2010). Methodology for sustainability strategic planning and management. Industrial Management & Data Systems, 110(2), 249-268. [ Links ]

Mantegui, N. & Zohrabi, A. (2011). A proposed comprehensive framework for formulating strategy: A hybrid of balanced scorecard, swot analysis, porter`s generic strategies and fuzzy quality function deployment. Procedia Social And Behavioral Sciences, Vol. 15, 2068–2073. [ Links ]

Pastor Tejedor, J. (2008). Modelo de gestión de calidad en instituciones sanitarias. Madrid: Ces, Consejo Economico Y Social. [ Links ]

Rezaei, A. R., Çelik, T. & Baalousha, Y. (2011). Performance measurement in a quality management system. Scientia Iranica, 18(3), 742–752. [ Links ]

Tohidi, H., Jafari, A. & Azimi Afshar, A. (2010). Using balanced scorecard in educational organisations. Procedia Social and Behavioral Sciences, 2(2), 5544–5548. [ Links ]

Yang, C. C. (2009). Development of an integrated model of a business excellence system. Total Quality Management, 20(9), 931-944. [ Links ]

Article history

Submitted: 31 May 2013

Accepted: 28 November 2013

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}