Serviços Personalizados

Journal

Artigo

Inglês (pdf)

Inglês (pdf)

Artigo em XML

Artigo em XML Referências do artigo

Referências do artigo

Enviar este artigo por email

Enviar este artigo por emailIndicadores

-

Citado por SciELO

Citado por SciELO -

Acessos

Acessos

Links relacionados

-

Similares em

SciELO

Similares em

SciELO

Compartilhar

Permalink

PermalinkEconomia Global e Gestão

versão impressa ISSN 0873-7444

Economia Global e Gestão vol.17 no.1 Lisboa abr. 2012

The COTEC Innovative SME Network from an economic and financial perspective

Paulo Bento*, Helena Pindo De Sousa** & João Oliveira***1

* Doutorado em Ciências de Gestão (The University of Manchester). Diretor (Revista Economia Global e Gestão). Subdiretor (Departamento de Marketing, Operações e Gestão Geral – ISCTE Business School). Coordenador (Audax-IUL). Investigador (Business Research Unit). E-mail: paulo.bento@alumni.mbs.ac.uk

** Mestre em Finanças (London Business School). Professora Auxiliar Convidada (ISCTE Business School). Diretora de Qualidade e Inovação (Agência Nacional de Compras Públicas). E-mail: hdesousa.mifft2000@london.edu

*** Mestre em Finanças (London Business School). Consultor Financeiro. E-mail: joliveira.mifft2001@london.edu

ABSTRACT

This article examines the COTEC Innovative SME Network from an economic and financial perspective. The COTEC Network is a group of companies that strives to be a reference for value creation in Portugal by adopting innovative attitudes and undertaking innovative activities. This analysis is made at the Network and sector levels. Portugals non-financial SMEs (at the national level) are the benchmark for the Network, and the non-financial SMEs for each economic sector in the country are the benchmark for the COTEC sectors. Although the conclusions require confirmation in future research, they indicate that companies in the Network have much higher levels of economic profitability and financial robustness than Portugals SMEs in general, both as a whole and by sector.

Keywords: Corporate Finance, Network, Innovation, SME, COTEC

Perspetiva económico-financeira da Rede PME Inovação COTEC

RESUMO

Este artigo efetua a caraterização económico-financeira da Rede PME Inovação COTEC, um grupo de empresas que pretende ser uma referência de criação de valor em Portugal, em resultado da adoção de atitudes e do desenvolvimento de atividades inovadoras. A análise faz-se a dois níveis: Rede e setores. No caso da Rede, o benchmark são as PMEs não financeiras do País, enquanto no caso dos setores são as correspondentes PMEs não financeiras. As conclusões, que carecem de confirmação em futuras investigações, apontam no sentido de as empresas da Rede terem níveis de rentabilidade económica e de robustez financeira muitíssimo acima da generalidade das PMEs em Portugal, tanto em termos globais como sectoriais.

Palavras-chave: Finanças Empresariais, Rede, Inovação, PME, COTEC

INTRODUCTION

This introduction is divided into three parts: the presentation of the COTEC Innovative SME Network (henceforth Network); aim and scope of the study; data and methodology.

Presentation of the Network

COTEC Portugal– Associação Empresarial para a Inovação is a corporate association for innovation, and its membership includes some of the most proactively innovative Portuguese companies. Set up in 2003 as part of a Presidency of the Republic initiative, it has currently more than one hundred associate companies (henceforth associates)2. The association has four main activity areas: i) knowledge enhancement; ii) sustained development of corporate innovation; iii) innovative SMEs; and iv) cross-sectional projects3. The Network was set up in 2005 under the third of these areas.

The Network is the object of analysis of this article. It was created for the development of SMEs skills and has the following goals: i) to establish cooperation among Network members (henceforth members), as well as between members and associates; ii) to provide specific support in growth stages, notably by attracting investment and supporting internationalization; iii) to promote public awareness of a group of SMEs whose innovative attitude and activity make them examples of value creation for Portugal4. The Network was initially formed with 24 companies and its membership has increased five-fold in five years.

Companies with an annual turnover of over two hundred thousand Euros can apply to become members of the Network. An evaluation committee, created specifically for this purpose, deliberates on the application and their decision is reached using an online system of Innovation Scoring (IS)5; this system is also used for the annual reassessment of membership status. The membership fee is the same for all members.

Aim and Scope of the Study

The economic and financial characterization of the Network, which is the aim of this article, fits into one of the three objectives defined when the Network was created. In fact, this exploratory article6 is intended to be another input to understanding the Network and could further contribute to consolidating its position as a reference for economic profitability and financial strength. Specifically, we will seek to understand how the economic and financial indicators of the Network compare with those of similar Portuguese companies, both as a whole and by sector.

Although other levels of research were considered, the final stratification and analysis address only the Network and Sectors7. Comparisons were made at each level against a benchmark built from the Sector Tables of the Central Balance Sheet Database of Banco de Portugal (henceforth CBSD), as follows: 1) Network vs. universe of non-financial SMEs (henceforth Country); 2) Members distributed by CAE8 Sections vs. Country distributed by CAE Sections. Average values for the Network and median values for the CBSD were used. The period covered in both cases is 2006 to 2008.

The two levels of analysis are addressed separately and with different depths, following the presentation of the data and brief methodological notes. The article ends with a set of remarks that aim to consolidate and, in some ways, complement the previous perspectives.

Data and Methodology

From this point on, Network refers to the 118 members that had a valid IES9 for the period under analysis, as opposed to the full set of members.

Several possibilities were considered for the definition of the sectors, some of which are popular but more subjective; however, the decision was made to use the CAE as this is a more solid and mature form of grouping, which has been revised and updated several times.

Sections were chosen from the various levels of CAE, denoted by a letter of the alphabet. Sections with three members or less were excluded10; as a result, 112 members were combined and the following sections used: C (Manufacturing), F (Construction), G (Wholesale and retail trade; repair of motor vehicles and motorcycles – henceforth Trade and Repair), J (Information and communication activities – henceforth ICT11), and M (Consulting, scientific, technical, and similar activities – henceforth Consulting).

With a view to improving the comparability and strength of the analysis, care was also taken to identify a database that was not only an appropriate benchmark for the possible levels of the analysis, but also credible, public, and free of charge. All things considered, the CBSD was chosen.

The measures used for benchmarking include the following indicators: profitability (Return on Equity and Operating Profit Margin), financial structure (Equity Ratio and Fixed Assets Coverage), liquidity (Current Ratio and Quick Ratio), operations (Asset Turnover and Inventory Turnover), investment (Investment Rate), and value added (Gross Value Added Rate). Any indicators that were not available in the CBSD or the IES, or that could not be calculated from these sources were excluded.

The methodology proposed by the Banco de Portugal was used to build the indicators so that comparisons could be made against the benchmarks in the CBSD, as summarized in Table 1.

TABLE 1

Indicator definition

CHARACTERIZATION OF THE NETWORK

Overview

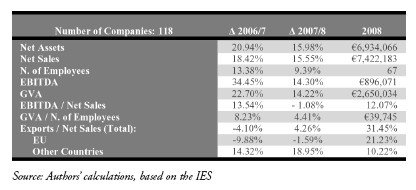

Table 2 shows that in 2008 the average company in the network had Net Assets of roughly 7 million Euros (m) and Net Sales of nearly 7.5m, almost one third of which were exports. Whereas the number of workers (67) would classify the average company as medium sized12, its Net Assets and Net Sales could categorize it as small. On average, each worker generated about 40 thousand Euros (k) of GVA annually (23k in the Country). It was therefore quite an agile and productive company in the national context, with a sizeable export component.

Summary characterization of the Network

Throughout the period under analysis, the key indicators characterizing the Network had a very positive evolution. For example, Net Sales grew by 36.8%, coupled with 53.7% growth in EBITDA. However, there were signs that this growth was not without difficulty. In effect, the inversion of the trend in the EBITDA margin (i.e. EBITDA/Net Sales) in the last year reveals a negative evolution that suggests some difficulty in managing corporate growth.

Profitability

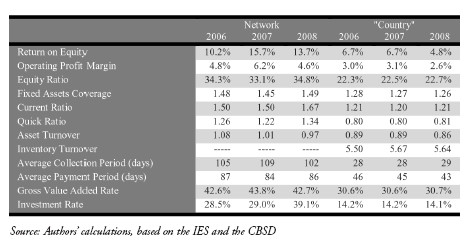

Table 3 shows that the Networks Return on Equity was significantly higher than that of the Country, demonstrating a more successful capital allocation towards positive Net Present Value projects. Specifically, the Networks Return on Equity (15.7%; 13.7%) in 2007 and 2008 was more than double that of the Country (6.7%; 4.8%). However, the trend for this indicator was negative between those two years, probably as a result of the outset of the current period of significant economic and financial turbulence.

Economic and financial indicators: Network vs. Country

From a strictly operational point of view (i.e. isolated from the financial and fiscal effects), the analysis of Operational Profitability confirms the interpretation of the previous indicator. It reveals the dynamic character of the Network and its unequivocal and substantial superiority (4.8%; 6.2%; 4.6%) compared to the Country (3.0%; 3.1%; 2.6%). In this context, the upward trend of this indicator was also clearly interrupted for both the Network and for the Country in the last year of the analysis, placing it below the 2006 level.

Financial Structure

It can also be seen from Table 3 that the Network had a much higher Equity Ratio (33.1% to 34.8%) than the Country (22.3% to 22.7%), which denotes a sounder and more balanced financial structure. This indicator also reveals that the companies in the Network financed projects more independently, i.e. had a greater capacity to raise own funds (including the reinvestment of the companys retained earnings) to support business initiatives. Variations in trends for both the Network and the Country were negligible during the period under analysis.

Fixed Assets Coverage is the best indicator to demonstrate compliance with the golden rule of financial equilibrium13 from a long term perspective; it should be higher than one in order for the minimum equilibrium to exist. This level of prudence was respected in both the Network and the Country, though the Networks level was higher, which is to some extent explained by the stronger Equity structure.

Liquidity

Table 3 also shows that the Networks liquidity level for both indicators was always greater than 1 in all years under analysis. The same cannot be said of the Country; its liquidity levels are not only lower than those of the Network but they are also lower than one for the Quick Ratio.

The Network is therefore understood to have better liquidity levels than the Country, and to be better prepared to face difficult situations such as the worlds current credit crunch14. We note that a liquidity level consistently higher than one can also mean a cash-absorbing operating cycle, especially if the indicator is growing as was the case for the Network in the period under analysis.

Operations

Table 3 further illustrates that the Networks Asset Turnover was higher than that of the Country; moreover, not only did the ratio decrease (albeit slightly) but it did so at a higher rate than that of the Country. In 2008, the Networks Asset Turnover was in fact lower than one, i.e. it was not possible to generate one euro of Net Sales for each euro of Assets, as was the case before. This development can indicate that Network companies had some difficulty in maintaining their historical efficiency levels in combination with their growth15. Indeed, it can be seen that the significant increase in the Networks Net Sales between 2006 and 2008 was accompanied by an even greater growth in Net Assets during the same period. This is in line with the strong Investment Rate observed.

On the other hand, the Inventory Turnover ratio provides specific information on the level of inventory necessary to support Net Sales16. For the Network, it is only meaningful to analyze this indicator at the section level (and then only in a few cases). In fact, as half of the 118 members mainly undertake service activities17, where typically the inventory levels are minimal or non-existent, the calculation of this indicator is clearly severely distorted.

The Average Collection Period and the Average Payment Period must be balanced to ensure rigorous management of working capital. Firstly, it must be noted that the former ratio for the Network is higher than the latter, resulting in net working capital requirements that need to be financed through some means other than credit from suppliers. Secondly, the operating cycle of the Network is substantially longer than that of the Country, indicating two of the Networks characteristics: i) stronger bargaining power relative to Suppliers and ii) weaker bargaining power relative to Clients (consistent with the increase in liquidity values), which does not necessarily mean a poor portfolio of commercial credits. During the period under analysis there was no significant change in the average collection and payment periods.

Investment and Value Added

Lastly,Table 3 demonstrates that the Networks Gross Value Added Rate (about 43%) was substantially higher than that of the Country (about 31%). In both cases, it was stable throughout the period. This is in line with what was mentioned for the GVA per worker, an indicator where the Network was also clearly more positive than the Country.

The Networks Investment Rate (around 30% to 40%) was more than double that of the Country (below 15%) in clear demonstration of an overall strategy based on growth and long term forcefulness, which is patent in the other ratios that were analyzed.

CHARACTERIZATION OF THE NETWORK BY SECTION

Moving on to the second level of the analysis, we try to ascertain to what extent the supremacy of the Network relative to the Country benchmark is confirmed at the level of the selected sections (Manufacturing; Construction; Trade and Repair; ICT; Consulting).

The structures of Table 2 and 3 have been replicated for the sections (Tables 4 to 13) but a less detailed analysis of the five sections is presented here. For each of the sections, we present only the highlights: first those relative to individual characterization (sometimes with comparisons to the whole Network), followed by the results of the comparison against the benchmark.

Summary characterization of Section C of the Network

Economic and financial indicators of Section C

Summary characterization of Section F of the Network

Economic and financial indicators of Section F

Summary characterization of Section G of the Network

Economic and financial indicators of Section G

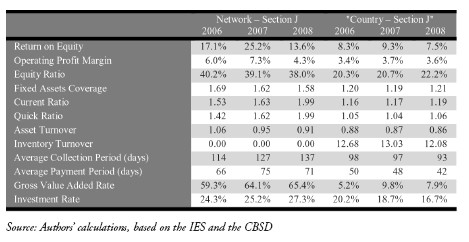

Summary characterization of Section J of the Network

Economic and financial indicators of Section J

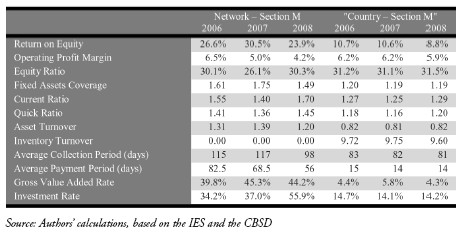

Summary characterization of Section M of the Network

Economic and financial indicators of Section M

Manufacturing

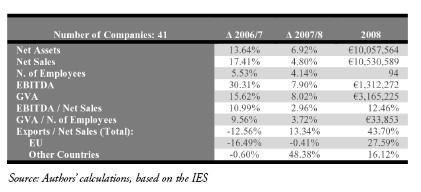

Section C was the most represented in the Network, with 41 members (more than a third of the total) – see Table 4. The average company is larger than that of the whole Network (Net Assets, Net Sales, and number of employees) and markedly more exporting (43.7% versus 31.45%), with an increasing focus on countries outside the EU.

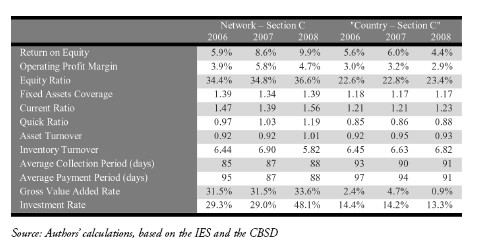

These members are more profitable than the benchmark and have quite a sound financial structure which allows them to engage in significant investment – see Table 5. There was considerable growth during the period, which did not originate imbalances, since the main ratios evolved positively. Generally, the economic and financial indicators have undoubtedly higher values than those of similar companies outside the Network. The financial management of the operating cycle appears to be the specific difficulty of these companies, especially in the last year under analysis.

Construction

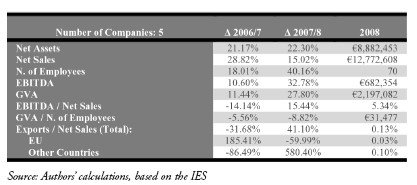

Section F included only 5 members of the Network, prompting caution in the interpretation of the data. Nevertheless, it should be noted that despite representing 4% of companies, their weight in Net Sales was 7% of the total and yielded the highest average – see Table 6. On the other hand, exports were negligible and subcontracting was about 16%.

The progress of the indicators during the period under analysis was quite favorable. Although labor productivity was the exception, the less favorable progress and low values are in keeping with a sector where low skilled labor predominates. Even so, it was more than 50% above the benchmark.

The profitability provided to equity holders was attractive (the second highest in the Network) and significantly higher than that of the benchmark – see Table 7. The strong Investment Rate (partially funded by debt) caused a decrease in the Equity Ratio, but without falling below the benchmark levels.

The efficiency of asset management was also better than that of peers outside the Network. However, treasury management was sometimes unfavorable, indicating difficulties in the management of debt collection and even sales, which were aggravated with the deepening of the crisis.

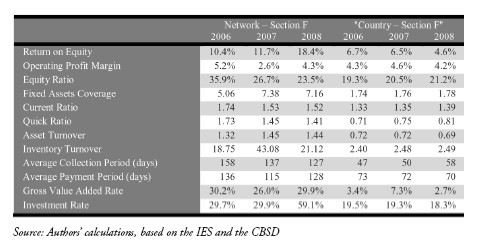

Trade and Repair

Section G had only seven members. On average, these employed 36 people and generated Net Sales of 5.6m, the second lowest of the five sections analyzed – see Table 8, to which the reservations for the previous sector apply. The year 2007 was poor, with falls in Net Sales, EBITDA margin, and labor productivity. Despite the strong recovery in 2008, which compensated for the previous year, this was the only sector for which all values without exception were below the Network average.

The benchmark revealed an unattractive sector, and the Networks members could hardly escape that reality. Nevertheless, they managed to show interesting dynamics and to reward their equity holders well beyond their peers outside the Network. In fact, outperforming the benchmark indicators was the rule – see Table 9.

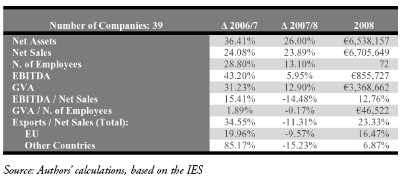

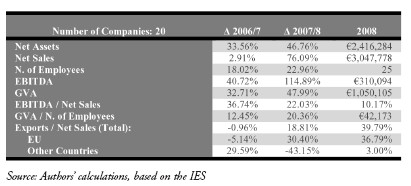

ICT

Section J represented about a third of the Network according to number of members and had the highest EBITDA margin and labor productivity, which was well above the productivity of the benchmark – see Table 10. The typical company could only be considered medium size in terms of the number of workers (72), since Net Sales and Net Assets (both around 6.5m) were those of a small company and below the general average of the Network.

Net Sales grew by 54% between 2006 and 2008, making it the sector with the second highest growth. Although exporting was not one of the strongest components, it represented nearly a quarter of Net Sales.

Network members performed better than their peers in the rest of the country in all respects: they were more profitable, they were financially stronger, they were more efficient, they had more liquidity, and they added more value to the economy – see Table 11.

Consulting

Section M was the third largest in the Network, with 18% of the members. The standard company was small, with 28 people and Net Sales of about 3m (the lowest in the Network, but of which about 40% originated overseas, making Consulting the second most exporting sector) – see Table 12.

These companies showed strong growth in both Net Sales (81%, the highest) and Net Assets (96%, the highest) during the period under analysis. They also had the best Return on Equity of the five sectors considered (well above the benchmark), the second highest productivity (again well above the benchmark), and a truly remarkable Gross Value Added Rate and Investment Rate (ridiculing the benchmark rates) – see Table 13.

CONCLUDING REMARKS

In the interest of clarity, the concluding remarks will follow the three part format used in the introduction: foreword; remarks; limitations and future research.

Foreword

In light of what has been said and the way in which the article was structured, we have chosen to present a set of remarks that aim to consolidate and, in some ways, complement the previous analyses.

To support this option, we have built Table 14, where the figures relate only to the most recent year, and are shown as indices, obtained by calculating the ratio between the value for the Network, or for each section of the Network, and their respective benchmarks. As for interpretation, whenever the value is above one, the performance of companies in the Network, or Network Section, is better than that of the companies in the benchmark; the reverse is true for values below one18. The transformation into indices introduces additional comparability and thus improves these remarks by allowing the comparison between sections, and between these and the Network as a whole.

TABLE 14

Network and sections vs. respective benchmarks (2008)

As previously stated, the validity of the absolute indicators and the ratios should be viewed with caution in Construction and Trade and Repair sectors given their small number of Network members. Therefore, attention focuses here only on the Network and the other three sectors.

Remarks

Generally, the indicators of companies in the Network, both as a whole and by sector, were always more favorable than their national peers, with only two exceptions: the Operating Profit Margin and Equity Ratio in Consulting were below the benchmarks.

Comparing the overall performance of the three sectors based on their relative distance from other companies in the Country, the values for ICT were the most extreme (four of the ten indicators were the most distant and five were the least distant). The least extreme positions were in Manufacturing, for which the distance was the greatest in three cases and the smallest in only one case. Lastly, the gap between the Network and its benchmark (Country) was higher than that of any sector (recall that we are excluding Construction and Trade and Repair) in three of the nine variables: Net Sales, Return on Equity, and Operating Profit Margin.

The analysis shows that Net Sales is the indicator in which the Network and the sectors are most distinct from their benchmarks, with values about ten or more times higher. The values of the Network and the sectors for Return on Equity and Investment Rate were almost treble those of their peers in the Country.

The economic profitability and financial strength of Network companies was generally well above that of the benchmark companies. Their management of available resources was more efficient; they had greater liquidity, and greater propensity for investment. Later, these would translate into better returns for investors as well as lower risk for debt holders.

Turning to sectors, the Network companies in the Manufacturing sector were more profitable than the companies in the benchmark; they also had a much sounder financial structure, which allowed them to undertake significant investments.

The ICT companies in the Network had better performance than their peers in all factors analyzed, despite a significant setback in 2008 (perhaps because of the onset of the crisis and their exposure to other markets): they were more efficient, had more liquidity, were more profitable, were financially stronger, and generated more added value.

Although Consulting was the only sector where the values for Network companies were below the benchmark (in two variables), these companies had the best Return on Equity of the five sectors analyzed, as well as a quite remarkable Gross Value Added Rate and Investment Rate. In fact, the Consulting companies in the Network had the best overall performance in the indicators selected for analysis in this study.

Limitations and Future Research

Testing the extent to which the economic profitability and financial strength of the companies in the Network is a cause or a consequence of the innovating attitude and activities, and thus make them examples of value creation, is an interesting avenue for future research. Possible hypotheses are: i) the innovation activity undertaken by the members depends on their initial economic and financial situation; ii) the innovation activity undertaken by the members influences their future economic and financial situation.

Such research would have to overcome the difficulties encountered in the present study, namely: i) insufficient detail on some of the economic and financial information, especially pertaining to R&D investment, R&D&I investment, and Net Sales from products and services resulting from the organizations R&D&I; ii) limited time frame of economic and financial data, which not only prevented a more robust analysis but also made it unfeasible to explore leads and lags with IS data due to doubts raised over the reliability of the latter.

REFERENCES

BANCO DE PORTUGAL, http://www.bportugal.pt/pt-PT/Paginas/inicio.aspx, 16.10.2011. [ Links ]

BREALEY, R. A.; MYERS, S. C. & ALLEN, F. (2011), Principles of Corporate Finance. McGraw-Hill, 10th ed., p. 944. [ Links ]

COTEC PORTUGAL, http://www.cotecportugal.pt/, 16.10.2011. [ Links ]

NOTES

1 This article has in its origin a subset of a much wider unpublished study, which was developed for COTEC by a consortium formed by specialists from ISCTE-IUL and ISEG, with the goal of characterising the innovation activity developed by the COTEC Innovative SME Network. Two of the authors of this article were the consortium members responsible for the component of that study which originated this article; however, it is more than justifiable to show gratitude to the remaining consortium members, in particular Pedro Camilo, Nuno Crespo and Vítor Corado Simões. Finally, acknowledgements are also due to the COTEC team, in particular Isabel Caetano and Carlos Cabeleira, who actively interacted with the consortium.

2 http://www.cotecportugal.pt/index.php?option=com_advassociates&Itemid=106, 16.10.2011.

3 http://www.cotecportugal.pt/index.php?option=com_content&task=blogcategory&id=72&Itemid=112, 16.10.2011.

4 http://www.cotecportugal.pt/index.php?option=com_content&task=blogcategory&id=58&Itemid=179, 16.10.2011.

5 http://www.innovationscoring.pt/, 16.10.2011.

6 This article is avowedly exploratory, because of the limitations mentioned in the end, while at the same time suggesting leads for future research. For reasons of space and respect for the reader, the details are omitted. These are presented in the much wider scoped study, which is unpublished.

7 The expressions section and sector, or their plurals, are used interchangeably.

8 Stands for Classificação das Atividades Económicas, the Portuguese Standard Industrial Classification.

9 Abbreviation for Informação Empresarial Simplificada, i.e. Simplified Business Information. IES is a recent process for companies to deliver information to public services, by using a dematerialized procedure – first data reported for the fiscal year of 2006. By submitting the IES files online, companies fulfil, at once, four different obligations: 1) Deposit of annual accounts in the Commercial Registry of the Ministry of Justice; 2) Delivery of annual fiscal declaration to the Ministry of Finance and Public Administration; 3) Delivery of annual information to the National Statistics Institute; 4) Delivery of information to the Portuguese Central Bank.

10 In order to avoid subjective or arbitrary criteria, we adopted a procedure identical to the one used by Banco de Portugal in the CBSD.

11 Although information and communication activities is not perfectly synonymous with information and communication technologies, the fluidity of exposure is improved by using the ICT buzzword, instead of creating a new acronym such as ICA.

12 The definition of medium sized company used here follows the classification of micro, small, and medium sized companies set by Recommendation 2003/361/CE, of 6 May 2003.

13 The golden rule of financial equilibrium states that a companys assets should be financed with capital having a maturity equal to or longer than the economic life of the assets.

14 There are various risks associated with liquidity, ranging from the loss of good business opportunities to bankruptcy, making its analysis very relevant. Ideally, Liquidity indicators should be higher than one, but this interpretation should be cautious and take into account the specificities of different companies and sectors, which is done in the following analysis.

15 Generally, the higher the Asset Turnover, the more efficient the management of the available resources is in generating economic profit.

16 As with Asset Turnover, generally the higher the value of this indicator, the higher the efficiency of inventory management.

17 Included here are the 39 members in section J and the 20 members in section M.

18 As an example, the value 12.71 allows the conclusion that companies in the Network have Net Sales 12.71 times higher than that of companies in the benchmark, which are the non-financial SMEs in the Country.