Serviços Personalizados

Journal

Artigo

Inglês (pdf)

Inglês (pdf)

Artigo em XML

Artigo em XML Referências do artigo

Referências do artigo

Enviar este artigo por email

Enviar este artigo por emailIndicadores

Citado por SciELO

Citado por SciELO Links relacionados

Similares em

SciELO

Similares em

SciELO Compartilhar

Permalink

PermalinkEconomia Global e Gestão

versão impressa ISSN 0873-7444

Economia Global e Gestão vol.17 no.3 Lisboa set. 2012

Expanding the core insight of microfinance lending groups: towards a new multilevel framework

Expandindo o insight fundamental dos grupos de empréstimo de micro finança: em direção a um novo framework multinível

Diego Marconatto*, Luciano Cruz** & Eugenio Pedrozo***

* PhD candidate at Federal University of Rio Grande do Sul, Brazil. His main research interests are microfinance, sustainable development and the role of institutions for poverty alleviation. E-mail: dmarconatto@gmail.com

** PhD from Jean Moulin Lyon 3 University. Associate Professor at HEC Montréal – courses on Corporate Social Responsibility and Sustainable Development in the Bachelor, MBA and Master degrees. E-mail: luciano.barin-cruz@hec.ca

*** PhD from INPL, Institut National Polytechnique de Lorraine, Nancy, France. Professor of Strategy, Interorganizational Relationships and Sustainable Innovation at Federal University of Rio Grande do Sul, Brazil. E-mail: eapedrozo@ea.ufrgs.br

ABSTRACT

The lending groups (LGs) have been created upon the insight that their arrangement has the capacity to reduce the information asymmetry and enforcement problems which drive poor borrowers out of traditional banks. We aim to expand on this insight, proposing that the success of LGs depends not only on their structural arrangement, but also on the positive configuration of their macro (institutional environment), meso (borrowers social networks) and micro contextual levels (cognitive frameworks of borrowers and microfinance institutions (MFI)s key workers). We present seven effects that connect all three levels in a tentative multilevel framework and provide a real example of how the model works.

Key words: Lending Groups, Microfinance, Multilevel Framework

RESUMO

Os grupos de empréstimos (GEs) foram criados a partir do insight de que seu arranjo possui a capacidade de reduzir os problemas de assimetria de informação e de enforcement, os quais excluem os tomadores de crédito mais pobres dos bancos tradicionais. Neste artigo, objetivamos expandir este insight ao propor que o sucesso dos GEs não depende apenas do seu arranjo estrutural, mas também da configuração positiva de seus níveis contextuais macro (ambiente institucional), meso (a rede social dos seus tomadores de crédito) e micro (os quadros cognitivos dos tomadores de crédito e dos trabalhadores-chaves da IMF). Nós apresentamos sete efeitos que conectam todos os três níveis em uma primeira sugestão de um framework multinível. Por fim, apresentamos um exemplo real que demonstra o funcionamento deste framework.

Palavras-chave: Grupos de Empréstimo, Micro Finança, Framework Multinível

INTRODUCTION

Microfinance is considered a key tool in poverty alleviation and sustainability strategies set up around the world (UN, 2005). In the last few decades, thousands of microfinance institutions (MFIs) began operation in many different countries, targeting millions of poor families formerly excluded from any kind of financial service (Mix Market, 2012). The lending groups (LGs) methodology lies at the heart of this astonishing rise in the number of the microfinance initiatives in place worldwide (Morduch, 1999; Yunus, 2007, Khavul, 2010), and has drawn a tremendous amount of attention from scholars and practitioners (Bhatt and Tang, 1998).

The methodology consists of a collective arrangement formed amongst low income borrowers which renders them all jointly responsible for repayment of the total group, non-collateralized, loan (Bhatt and Tang, 1998; Khavul, 2010; Morduch, 1999). In other words, if one borrower defaults, the other borrowers who comprise the LG must repay his overdue obligation, or risk having further loans denied by the MFIs if they fail to do so.

The LGs methodology is founded upon a core insight: it is believed that the socio-institutional micro arrangement of LGs allows them to reduce the information asymmetry and enforcement problems which have historically driven low income borrowers out of the traditional banks (Anderson et al. 2002; Bastelaer, 1999; Guinanne and Ghatak, 1999; Khavul, 2010; Morduch, 1999; Robinson, 2002). The LGs accomplish this through the improvement of the performance of the three activities directly associated with reducing information asymmetry and enhancing enforcement: screening, monitoring and enforcement (SME activities) (Morduch, 1999). Thus, the superior performance of these three reduction risk activities is the raison dêtre of LGs.

However, an ongoing line of research (Bhatt and Tang, 1998; Cassar et al., 2007; Hung, 2003, 2006; Wenner, 1995; Wydick, 1999) has provided evidence that this collective arrangement per se may not always improve the SME activities as expected. These studies have shown that the success of this collective arrangement depends not only on the internal configuration but also on a myriad of factors diffused throughout the macro (MFIs institutional environment), meso (borrowers social networks) and micro (borrowers cognitive frameworks and MFIs key workers) levels of the LGs context. Nevertheless, little has been done in the previous literature to systematize the reciprocal relationships of these levels and their main effects on the SME activities performed by the LGs.

Based on these arguments, we propose a theoretical shift in the LGs core insight, providing a tentative multilevel framework for the SME activities. We will argue in this paper that the capacity of the LGs to perform the SME activities depends not simply on their internal configuration, but rather on the coordination of the inter-effects connecting the macro, meso and micro contextual levels which together embrace these groups. We will refer to the literature on women and repayment rate to provide a facts-based example of how seven identified inter-effects articulate the three above mentioned levels and affect the performance of the SME activities conducted by LGs.

The remainder of this article is organized as follows: first, we present our tentative multilevel framework for the risk reducing activities (SME) performed by LGs. Next, we explain seven key interrelations connecting the macro, meso and micro levels of the proposed framework, and their effects on the SME activities. Thirdly, we refer to the literature on MFIs female borrowers to show how the framework works. Finally, we discuss the implications of our framework and propose new lines of inquiry for the research and practice of LGs.

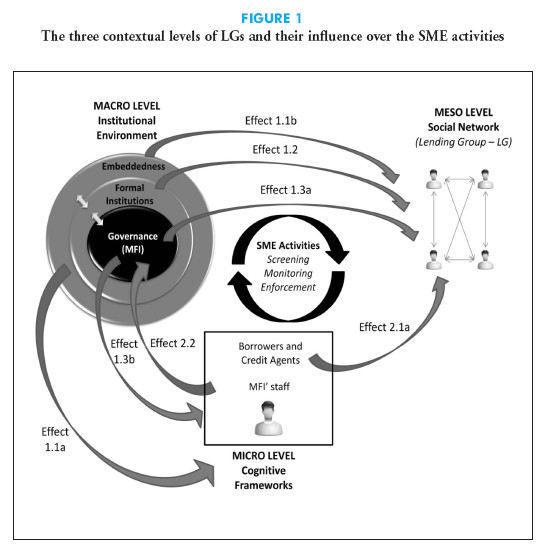

A MULTILEVEL FRAMEWORK FOR THE SME ACTIVITIES PERFORMED BY LGS

The effectiveness of LGs performance of the SME activities is anchored in and dependent upon elements of the overarching context within which these groups find themselves embedded (Bhatt and Tang, 1998). These elements can have different forms and natures and can be grouped around the three levels comprising the context of MFIs: macro level (MFIs institutional environment), meso level (the social networks of MFIs borrowers) and micro level (borrowers cognitive frameworks and MFIs key workers) (Beckert, 2010).

These three levels are in continuous and mutual interaction. As Beckert (2010) posits, they may reinforce each others current configurations or instead they may stir up and force mutual changes. In the MFI context, this means that the capacity of each level to improve or hinder the SME activities performed by LGs affects the other two levels positively or negatively, and at the same time is affected by them. In this paper, we identify seven main inter-effects related to the SME activities which connect these three levels. These effects might be orchestrated in such a way that all three levels converge for the maximization of the efficiency of the SME activities; alternatively, the seven effects might cause an overall negative influence over these three activities, reducing their efficiency.

Hence, we argue that the LGs capacity to perform the SME activities is determined by the overall configuration of the aforementioned three levels. We illustrate this proposition in Figure 1.

CONNECTING THE THREE LENDING GROUPS CONTEXTUAL LEVELS

In this section, we explain the seven inter-effects connecting the three LGs macro (institutional environment), meso (borrowers social network) and micro (borrowers cognitive frameworks and MFIs key workers) levels.

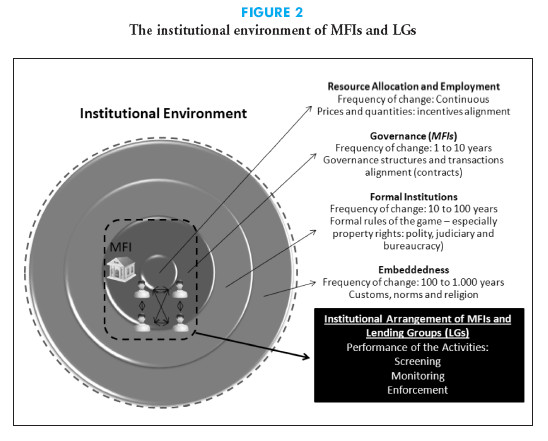

As depicted in Figure 2, the institutional environment is formed by four connected and overlapping circles (Williamson, 2000), of which the first three are the most important for our argument. The first is called the embeddedness circle and embraces culture, traditions, customs, norms and religion. These informal and deeply-rooted institutions influence the general levels of trust, commitment and cooperation pervading the society (Putnam, 1993). Therefore, the embeddedness circle might, on one hand, encourage a more unobstructed and stronger flow of information, the de-bureaucratization of economic and social transactions, and the use of social sanctions in addition to the legal sanctions prescribed by laws. On the other hand, archaic institutions might nurture a widespread feeling of insecurity that undermines trust and cooperation, obstructing the streams of social and economic information (North, 1991; Putnam, 1993). While the first scenario will facilitate the performance of the SME activities by the LGs, the second will hinder these same activities (Bhatt and Tang, 1998). Moreover, the embeddedness circle informs what is morally right and wrong for individuals and social groups (Williamson, 2000), and influences the definition of social roles, such as the hierarchical position of men and women in society. Therefore, we argue that:

Effects 1.1a and 1.1b: the SME activities performed by the (1.1a) borrowers, organized in LGs (1.1b) are affected by the embeddedness circle of the institutional environment. Its prevailing customs, social norms and values inform the borrowers and LGs about the desirable/accepted and undesirable/forbidden relational patterns regarding the screening, monitoring and enforcement of their peers. While trust-based, cooperative societies tend to bolster the SME activities, societies pervaded by a widespread feeling of insecurity, ruled by personalistic relationships, tend to hinder the performance of these three activities.

The embeddedness circle shapes the next layer of the institutional environment: the formal institutions regulating the society and the economy (e.g.: government, laws, and judiciary) (Williamson, 2000). Strong and stable formal institutions, such as those from the more developed countries, boost the diffusion of reliable and cost-efficient information throughout the markets and offer additional monitoring and enforcement power to their social collective arrangements (Choi et al., 2009; North, 1991), such as the LGs.

In contrast, many developing countries have their society and economy ruled by dysfunctional institutions which feed coercive, exploitative and dependent relationships between individuals (Putnam, 1993). Usually, this kind of environment also lacks efficient informational systems, has undermining flaws in its formal monitoring mechanisms and high levels of corruption and inconsistency in its sanctioning (enforcement) structures (Choi et al., 2009). In addition, these environments are usually gender-biased, which narrows the social and economic opportunities for women (Johnson, 2004). Thus, formal institutions in which the screening, monitoring and enforcement activities could be safely anchored are often lacking in this kind of context. Therefore, we argue that:

Effect 1.2: The SME activities performed by the LGs are affected by the formal institutions circle of the institutional environment. Screening, monitoring and enforcement activities are supported by strong, reliable and cost-efficient formal institutions and hindered by weak, unstable and inefficient formal institutions.

The institutional environment embraces a third layer: the governance circle (Williamson, 2000). Within the microfinance industry, the governance circle is substantiated by the different MFIs, which along with the LGs directly design and operate the SME activities. The MFIs spread over the world may follow one of the three orientations explained by Battilana and Dorado (2010): financial, social or sustainable. Each orientation is underpinned by different tenets which give rise to a particular design for the MFI structure, preferences and practices, including the design and performance of the SME activities. On the one hand, financially-oriented MFIs usually emulate the highly formalized philosophy and methods of traditional financial institutions (Dichter and Harper, 2007). These organizations seek profits and the eventual social gains accrued by their operations are considered as a collateral effect. The socially-oriented MFIs, on the other hand, are designed to help low income populations lift themselves out of poverty (Morduch, 2000; Woller et al., 1999). These organizations are recognized by the highly informal methods they use to screen and monitor their borrowers and enforce repayment (Brehanu and Fufa, 2008; Mersland, 2009; Wenner, 1995). The third group of MFIs, known as sustainably-oriented, strives to strike a balance between the financial and social orientations: fighting poverty while breaking even, therefore freeing themselves of external subsidies (Battilana and Dorado, 2010). According to the authors, these organizations may use a wide range of different methods, employed either by financially- or socially-oriented MFIs. Thus, we posit that:

Effect 1.3a: the SME activities performed by the LGs are affected by the governance circle (MFIs) of the institutional environment. The different orientations and designs of the MFIs will give rise to different methods and designs for the LGs and the SME activities.

Through their orientation, hiring and training systems, the MFIs define and shape the worker profile that will be engaged in the organization and, therefore, the belief system that will prevail inside the institution. While socially-oriented MFIs are usually operated by social workers and, not infrequently, activists, financially-oriented MFIs are managed by accountants and other financial executives (Battilana and Dorado, 2010). Sustainably-oriented MFIs tend either to hire both profiles of worker or to socialize them within a hybrid mindset. Each group will resemble their cognitive framework in the design and performance of the SME activities carried out by its MFI (Battilana and Dorado, 2010).

The MFIs orientation also has a direct impact on the definition of which type of borrowers these institutions will serve. Socially-oriented MFIs are likely to target the economically worst-off clients in the microfinance industry (Hishigsuren, 2007; Mix Market, 2012). These organizations also seem to have a stronger focus on the female public and other specific populations such as ethnic groups, villages struck by diseases (e.g., AIDS), immigrants, and refugees (Achola, 2006; Bhatt and Tang, 2001, 2002; DÉspallier et al., 2011; Mersland, 2009; Morduch, 1999a). In turn, financially-oriented MFIs target the higher bound of the poor populations (the poor-riches) (Dichter and Harper, 2007; Khavul, 2010; Yunus, 2007). This public can offer more fungible collateral, lower transaction costs and risks and thus make it easier maximize their revenues (Cull et al., 2009). Again, the sustainably-oriented MFIs may attend a higher range of target publics (Cull et al., 2009). These diverse target publics are expected to have different cognitive frameworks, relational attitudes, and different needs to be fulfilled by the three types of MFIs. Thus, we argue that:

Effect 1.3b: the cognitive frameworks of the MFIs key workers and borrowers are affected by the governance circle (MFIs) of the institutional environment. Through their orientation, the MFIs select and shape the cognitive frameworks of their staff, which will impact the design and performance of the SME activities. The MFIs orientation is also the criterion for the selection of the target public to be served by these organizations.

We now present the effects of the micro level (cognitive frameworks) on the two other levels. According to Ostrom (2000), individuals experiencing the same economic scenario cannot be expected to invariably make the same decisions. The same author states that there are many different types of economic agent – not just the classical rational-egotist agent: individuals may be more or less prone to collaborating with, monitoring, punishing and rewarding their peers involved in economical transactions.

These insights resonate within the microfinance literature. For instance, Hung (2003, 2006) found that the borrowers and lenders respond in different modes to the MFIs regulation of the SME activities. Ito (2003) showed how, despite the rules, some credit agents eventually help defaulting borrowers, even lending them money from their own pockets, impelled by prior existent friendship ties. Others, like Johnson (2004), suggest that moral hazard is gendered: female borrowers are less opportunistic than male borrowers. Therefore, we argue that:

Effect 2.1a: the SME activities performed by the LGs are affected by the cognitive framework of borrowers and MFIs key workers. The different attitudes they have towards risk, the varied responses they give to similar contextual rules and the different relational patterns they present among each other influence the performance of the SME activities.

The cognitive frameworks of the MFIs key workers and founders, in turn, affect the orientation and design of these organizations, including the SME activities. The MFIs orientation is initially shaped by the motivations and philosophy of the founding group (Battilana and Dorado, 2010). These founders usually exert a lasting and pervasive influence over the MFIs – that is why, for instance, MFIs founded and ruled by female CEOs are often female-gender biased (Mersland and Strøm, 2009). Yunus (2007) is perhaps the most remarkable example in the microfinance field. His philosophy has profoundly shaped not only his Grameen Bank – surely the most famous MFI in the world – but also a worldwide network of MFIs dedicated to easing the suffering of poor communities. It is from the founders vision that the SME activities will be tentatively outlined.

The MFIs key workers, in turn, may perpetuate or impose incremental or radical changes in the orientation and design of their hosting organizations. Small, community-based, MFIs founded upon an ideal of emancipation of their poor borrowers for example, may undergo radical changes when taken over by financially-minded workers focused on widely accepted performance indicators and efficiency measures. The new prevailing mindset may steer the MFI away from its initial mission towards more profitable lines of products and target publics, a phenomenon known as mission drift (Aubert et al., 2009; Battilana and Dorado, 2010; Getu, 2007; Morduch, 2000). Therefore, we argue that:

Effect 2.2: The MFIs orientation and design is affected by the cognitive framework of the MFIs key workers and founders. The ideology and background of the MFIs founder shape the drivers, methods and structure of the organization, including the SME activities. The MFIs key workers will perpetuate or incrementally or radically change these organizations and activities.

THE MULTILEVEL FRAMEWORK IN PRACTICE: THE INTERCONNECTION OF THE THREE CONTEXTUAL LEVELS OF LGs FORMED BY WOMEN

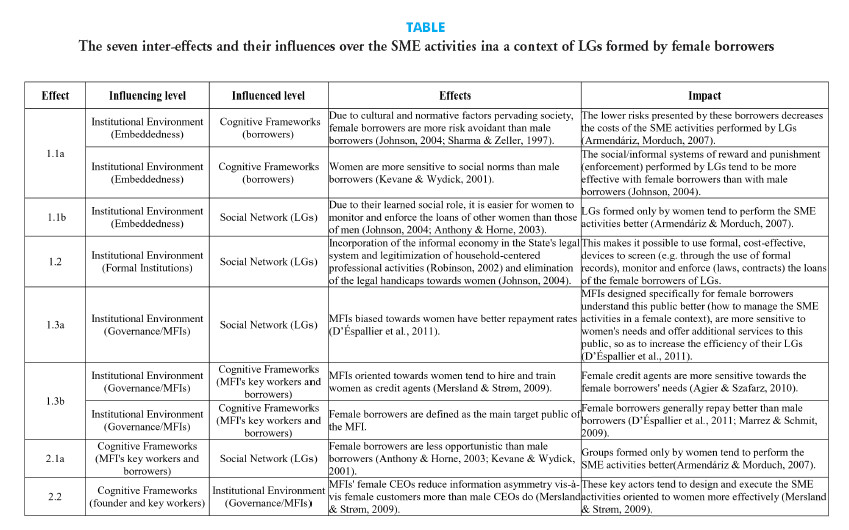

In this section, we reference the microfinance literature on the relationship between women and the repayment rate to provide an example of how the overall configuration of the seven aforementioned inter-effects influences the SME activities performed by female borrowers gathered in LGs. There are at least three reasons for basing this example on the case of female borrowers. First, women occupy a central role in the world of microfinance. Mody (2000) asserts that women account for more than 80% of the total clients of the worlds largest MFIs. In another example, the Grameen Banks female borrowers account for over 90% of its total clients (Houssain, 1998; Yunus, 2007). At the same time, most of the women taking out microloans around the world do so through LGs and other collective arrangements (Armendáriz and Morduch, 2007).

Second, female borrowers are believed to sustain better repayment rates than male borrowers (Armendáriz and Morduch, 2007; Houssain, 1988; Johnson, 2004; Kevane and Wydick, 2001; Sharma and Zeller, 1997; Yunus, 2007). Although this insight has long been rooted in the microfinance literature, D'Éspallier et al. (2011) claim to be the first authors to test this assertion on a global scale. Their results endorse womens superior repayment performance. However, as they affirmed, it is not yet clear which reasons are behind this phenomenon around the world. As we see in the Table, some authors directly relate the superior performance of women with the particular interaction they maintain with the SME activities.

Table

The third reason relates to the fact that microfinance has been considered an important tool to promote womens empowerment (Montgomery and Weiss, 2011; Morduch, 1999; Sanyal, 2009; Yunus, 2007). Therefore, a better understanding of how the macro, meso and micro levels of the context of LGs formed by women affect the LGs performance of SME activities is a crucial goal within the microfinance field.

We summarize our exemplification in the Table in which the effects depicted in Figure 1 and described in the third Topic are related to the relevant literature findings on female borrowers. Through the available evidence, we connect the influencing levels to the influenced levels of the LGs context, deriving the correspondent impacts on the SME activities.

Our example shows how a positive configuration of all the three contextual levels of LGs formed by women can influence each other, bolstering the efficiency of the SME activities. It also reveals that contrary to what is implied by the actual core insight enlivening microfinance, the success of these activities and, subsequently, of the LGs themselves relies not only on their internal arrangement. It relies on the overall interactions amongst the macro (MFIs institutional environment), meso (borrowers social networks) and micro (cognitive frameworks of borrowers and MFIs staff) levels of the LGs context.

DISCUSSION

In this paper, we proposed a theoretical shift in the core insight of lending groups (LGs), hitherto known as the most celebrated innovation in microfinance (Morduch, 1999, p. 1572). Referring to the evidence available in the microfinance literature, we suggested that the alleged capacity for increasing the performance of the three activities designed to lower the information asymmetry and ameliorate enforcement problems (Screening, Monitoring and Enforcement – SME) cannot be explained solely by the internal configuration of lending groups.

Through the substantiation of seven inter-effects, we showed that the LGs success depends upon their level of fitness, or positive accommodation, along with their micro, meso and macro contextual levels. Thus, we proposed the first multilevel framework for LGs that connects all the three levels. Our work has the following implications:

First, it evidences the need for scholars dedicated to the study of LGs to expand their focus from these groups themselves to the overall environment embracing them. This point had already been stressed by Bhatt and Tang (1998). However, these authors did not mention which environmental factors beyond the LGs should be taken into account.

Second, our multilevel framework sheds new light on the research and practice devoted to the transference of LGs methodologies around the world. The most well-known and frequently reproduced model of an LG is the one established by the Grameen Bank (Morduch, 1999). However, studies have shown that indiscriminate attempts to transfer this model to different contexts are not always successful (Hulme, 1991; Lavoie, 2009; Robinson, 2002). Among other reasons, the transference failures are credited to the lack of fit between the lending method and the economic and social reality of the recipient populations (Bhatt and Tang, 1998; Robinson, 2002). Hence, our multilevel framework may inspire scholars and MFIs executives to be more mindful about how best to accommodate the LGs methodology within the three contextual levels.

Third, our work may help practitioners to better evaluate whether LGs are the best lending method to be employed in a given context. This is important because despite all the faith in LGs, the available evidence does not confirm that their performance consistently surpasses that of other lending methods, such as individual loans (Wenner, 1995, Cull et al., 2009). The stunning success of the Grameen Banks LGs seems to have led to the naive assumption that they represent an infallible solution to the information asymmetry and enforcement problems characteristic of lending within poor populations. However, evidence has again suggested that, depending on the specific situation, the LGs may not always be the best option (Bhatt and Tang, 1998, 2001, 2002; DÉspallier et al., 2011; Morduch, 1999).

Finally, we encourage scholars to further develop our proposed model, refining and empirically testing it in different configurations of LGs and contexts. In this paper, we considered the seven most evident theoretical interrelations connecting the macro, meso and micro contextual levels of LGs. However, there may be other existent interrelations which were not taken into account in our model and that are ultimately important to a given LGs methodology or specific context.

REFERENCES

ACHOLA, P. (2006), Impact of HIV/AIDS on Microfinance: with a case study on HIV/AIDS mitigation. Mennonite Economic Development Associates, Montreal. [ Links ]

AGIER, I. & SZAFARZ, A. (2010), «Microfinance and Gender: Is There a Glass Ceiling in Loan Size?». Research Institute in Management Sciences, Brussels,Working Paper no. 10/047, pp. 1-38. [ Links ]

ANDERSON, C. L.; LOCKER, L. & NUGENT., R. (2002), «Microcredit, social capital, and common pool resources». World Development, 30(1), pp. 95-105. [ Links ]

ANTHONY, D. & HORNE, C. (2003), «Gender and cooperation: explaining loan repayment in micro-credit groups». Social Psychology Quarterly, 66(3), pp. 293-302. [ Links ]

ARMENDÁRIZ, B. & MORDUCH, J. (2007), The Economics of Microfinance. Cambridge, MIT Press. [ Links ]

AUBERT, C.; JANVRY, A. & SADOULET, E. (2009), «Designing credit agent incentives to prevent mission drift in pro-poor microfinance institutions». Journal of Development Economics, 90(1), pp. 153-162. [ Links ]

BASTELAER, T. V. (1999), «Does Social Capital Facilitate the Poors Access to Credit? A Review of the Microeconomic Literature». The World Bank, Washington, DC, Social Capital InitiativeWorking Paper, no. 8, pp. 1-24. [ Links ]

BATTILANA, J. & DORADO, S. (2010), «Building sustainable hybrid organizations: the case of commercial microfinance organizations». Academy of Management Journal, 56(6), pp. 1419-1440. [ Links ]

BECKERT, J. (2010), «How do fields change? The interrelations of institutions, networks, and cognition in the dynamics of markets». Organization Studies, 31(5), pp. 605-627. [ Links ]

BHATT, N. & TANG, S. Y. (2002), «Determinants of repayment in microcredit: evidence from programs in the United States». International Journal of Urban and Regional Research, 26(2), pp. 360-376. [ Links ]

BHATT, N. & TANG, S. Y. (2001), «Making microcredit work in the United States: social, financial, and administrative dimensions». Economic Development Quarterly, 15(3), pp. 229-241. [ Links ]

BHATT, N. & TANG, S. Y. (1998), «The problem of transaction costs in group-based microlending: an institutional perspective». World Development, 26(4), pp. 623-637. [ Links ]

BREHANU, A. & FUFA, B. (2008), «Repayment rate of loans from semi-formal financial institutions among small-scale farmers in Ethiopia: a two-limit tobit analysis». Journal of Socio-Economics, 37(6), pp. 2221-2230. [ Links ]

CASSAR, A.; CROWLEY, L. & WYDICK, B. (2007), «The effect of social capital on group loan repayment: evidence from field experiments». The Economic Journal, 117 (Feb), pp. 85-106. [ Links ]

CHOI, C. J.; KIM, S. W. & KIM, J. B. (2009), «Globalizing business ethics research and the ethical need to include the bottom-of-the-pyramid countries: redefining the global triad as business systems and institutions». Journal of Business Ethics, 94(2), pp. 299-306. [ Links ]

CULL, R.; DEMIRGÜÇ-KUNT, A. & MORDUCH, J. (2009), «Microfinance meets the market». Journal of Economic Perspectives, 23(1), pp. 167-192. [ Links ]

DÉSPALLIER, B.; GUÉRIN, I. & MERSLAND, R. (2011), «Women and repayment in microfinance: a global analysis». World Development, 39(5), pp. 758-772. [ Links ]

DICHTER, T. & HARPER, M. (2007), Whats Wrong with Microfinance? Practical Action, Warwickshire. [ Links ]

GETU, M. (2007), «Does commercialization of microfinance programs lead to mission drift?». Transformation, 24(3), pp. 169-180. [ Links ]

GUINNANE, T. W. & GHATAK, M. (1999), «The economics of lending with joint liability: theory and practice». Journal of Development Economics, 60(1), pp. 195-228. [ Links ]

HISHIGSUREN, G. (2007), «Evaluating mission drift in microfinance: lessons for programs with social mission». Evaluation Review, 31(3), pp. 203-260. [ Links ]

HOUSSAIN, M. (1988), «Credit for Alleviation of Rural Poverty: The Grameen Bank in Bangladesh». International Food Policy Research Institute, Washington, DC. Research Report, no. 65, pp. 1-96. [ Links ]

HULME, D. (1991), «The Malawi Mundi fund: daughter of Grameen». Journal of International Development, 3(4), pp. 427-431. [ Links ]

HUNG, C. R. (2003), «Loan performance of group-based microcredit programs in the United States». Economic Development Quarterly, 17(4), pp. 382-395. [ Links ]

HUNG, C. R. (2006), «Rules and actions: determinants of peer group and staff actions in group-based microcredit programs in the United States». Economic Development Quarterly, 20(1), pp. 75-96.

ITO, S. (2003), «Microfinance and social capital: does social capital help create good practice?». Development in Practice, 13(4), pp. 322-332.

JOHNSON, S. (2004), «Gender norms in financial markets: evidence from Kenya». World Development, 32(8), pp. 1355-1374.

KEVANE, M. & WYDICK, B. (2001), «Microenterprise lending to female entrepreneurs: sacrificing economic growth for poverty alleviation?». World Development,29(7), pp. 1225-1236.

KHAVUL, S. (2010), «Microfinance: creating opportunities for the poor?». Academy of Management Perspectives, 44(1), pp. 9-17.

LAVOIE, F. (2009), «Conditions Facilitating the Replication of Microcredit Methodologies». Master Thesis, HEC Montréal, Montréal.

MARREZ, H. & SCHMIT, M. (2009), «Credit risk analysis in microcredit: how does gender matter?». Research Institute in Management Sciences,Brussels, Working Paper no. 9, pp.1-20.

MERSLAND, R. & STRØM, R. Ø. (2009), «Performance and governance in microfinance institutions». Journal of Banking & Finance, 33(4), pp. 662-669.

MERSLAND, R. (2009), «The cost of ownership in microfinance organizations». World Development, 37(2), pp. 469-478.

MIX MARKET (2012), «Microfinance database». http://www.themix.org/about/microfinance.

MODY, P. (2000), «Gender Empowerment and Microfinance». University of Washington, Washington DC, Working Paper.

MONTGOMERY, H. & WEISS, J. (2011), «Can commercially-oriented microfinance help meet the millennium development goals? Evidence from Pakistan». World Development, 39(1), pp. 87-109.

MORDUCH, J. (1999), «The microfinance promise». Journal of Economic Literature, 37(4), pp. 1569-1614.

MORDUCH, J. (2000), «The microfinance schism». World Development, 8(4), pp. 617-629.

NORTH, D. (1991), «Institutions». Journal of Economic Perspectives, 5(1), pp. 87-112.

OSTROM, E. (2000), «Collective action and the evolution of social norms». Journal of Economic Perspectives, 14(3), pp. 137-158.

PUTNAM, R. (1993), Making Democracy Work: Civic Traditions in Modern Italy. Princeton University Press, New Jersey.

ROBINSON, M. S. (2002), The Microfinance Revolution: Sustainable Finance for the Poor. World Bank, Washington, DC.

SANYAL, P. (2009), «From credit to collective action: the role of microfinance in promoting womens social capital and normative influence». American Sociological Review, 74(4), pp. 529-550.

SHARMA, M. & ZELLER, M. (1997), «Repayment performance in group-based credit programs in Bangladesh: an empirical analysis». World Development, 25(10), pp. 1731-1742.

UNITED NATIONS CHRONICLE ONLINE EDITION (2010), http://www.un.org/Pubs/chronicle/2005/issue3/0305p45.html.

WENNER, M. D. (1995), «Group credit: a means to improve information transfer and loan repayment performance». The Journal of Development Studies, 32(2), pp. 263-281.

WILLIAMSON, O. E. (2000), «The new institutional economics: taking stock, looking ahead». Journal of Economic Literature, 38(3), pp. 595-613.

WOLLER, G. M.; DUNFORD, C. & WOODWORTH, W. (1999), Where to microfinance? International Journal of Economic Development, 1(1), pp. 29-64.

WYDICK, B. (1999), «Can social cohesion be harnessed to repair market failures? Evidence from group lending in Guatemala». The Economic Journal, 109(Jul), pp. 463-475.

YUNUS, M. (2007), Banker to the Poor: Micro-Lending and the Battle against Poverty. Public Affairs, New York.

{kind=link}